Dimitris Papanikolaou, Lawrence D.W. Schmidt 23 July 2020

The COVID-19 pandemic has led to unprecedented changes in how firms conduct their business. In response, policymakers have launched large government spending programmes to mitigate the harm done to the economy. Some of these policies, like the Paycheck Protection Program in the US, identically treat all firms that satisfy basic qualifying criteria despite the fact that not every sector was equally affected. Likewise, US households below an income threshold received stimulus checks regardless of their particular circumstances.

But are these strategies cost-effective? The lockdown policies intended to limit the spread of COVID-19 have shut down in-person work for almost all sectors of the economy, forcing their employees to work from home. As noted by Alon et al. (2020), there are considerable differences across sectors with respect to their ability to work remotely.

According to the American Time Use Survey, approximately 3% of workers who are employed in the transportation and material-moving sector can work remotely, while 78% of computer programmers can do so. To complicate matters further, some industries are classified as essential businesses and are allowed to remain open for in-person transactions, while others are not.

We use these two facts to isolate the supply-side impact of COVID-19 on different industries and to understand the heterogeneity that underlies the virus’s effects on the economy (Papanikolaou & Schmidt, 2020). Our findings are consistent with and complement the work of Barrero et al. (2020), as we find that supply-side disruptions are economically large and responsible for substantial dispersion in outcomes between workers and firms.

Quantifying the cost of being unable to work from home

Leveraging the American Time Use Survey data, we construct a measure of exposure to COVID-19 workforce disruptions at the industry level as

COVID-19 work exposure = 1 – (% of workers able to work from home).

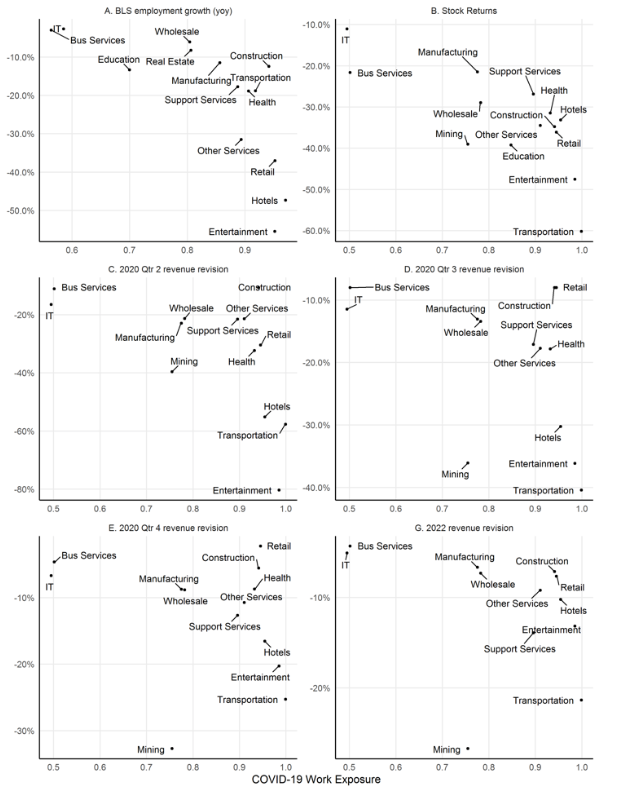

We find that the economic effect of the initial shock of shutting down the economy varied significantly across sectors. Across nearly all measures we looked at, firms in sectors in which most of the work could be done remotely fared much better than industries where employees needed to work on site (Figure 1).

Figure 1 Economic effect of COVID-19 exposure across industries

Notes: Panel A plots employment growth rates from April 2020 vs 2019 from the BLS against exposure (aggregated using BLS total employment weights). Panels B–F plot stock returns and revisions in revenue forecasts for non-critical industries from mid-February to mid-May versus the COVID-19 work exposure measure.

For instance, when we restrict attention to industries that are not classified as essential services, an increase of one standard deviation in our exposure metric is associated with a 10% decline in employment; an 8% decline in revenue forecasts for Q2 of 2020; an 0.22-percentage-point increase in default probability; and a 7% decline in stock market performance (year to date).

Further, these differences are likely to be persistent: analysts forecast a decline of annual revenues of 13, 10, and 8% for 2020, 2021, and 2022 for non-critical industries; for critical industries, those numbers are 3.2, 3.5, and 2.3%, respectively.

Recent survey data also bears bad news for non-critical firms exposed to supply-side disruptions. A change of one standard deviation in exposure is associated with a 9.4-percentage-point increase in the probability of experiencing a major disruption, a 5.7- and 4.0-percentage-point increase in the likelihood of reducing headcount and payroll, a 5.9-percentage-point increase in the probability of missing payments, and a 4.3-percentage-point increase in the likelihood of having insufficient liquidity.

Examining the outcomes for individual workers, a change of one standard deviation in exposure is associated with a 4.5-percentage-point increase in the likelihood that a worker in a non-critical industry is not employed, while a similar change in exposure is associated with only a 1.0-percentage-point increase in unemployment for a worker in a critical industry.

These average effects mask substantial dispersion across income, education, and gender. For workers in the bottom quartile of the earnings distribution in non-critical industries, unemployment sees a 9.2-percentage-point increase. For women with young children and no college degree, that number is 15 percentage points – three times higher than the average response across all workers.

These findings show that the reallocative effects of the work disruptions associated with the COVID-19 pandemic were quite substantial. To the extent that some workers may not be able to easily switch sectors, the resulting demand shock can be large (Guerrieri et al. 2020).

Real-time estimates of the disruption

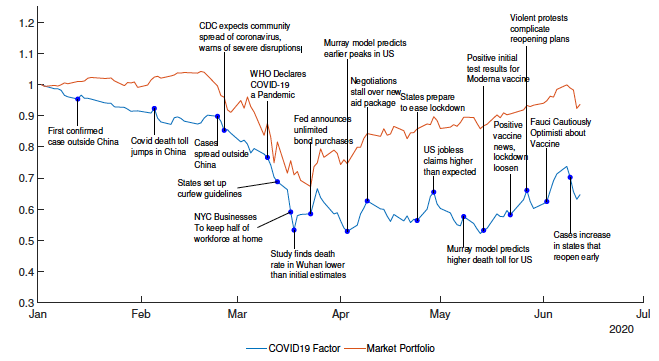

Information about the severity of the COVID-19 pandemic was released over time. By looking at high-frequency measures of outcomes, we can get a better sense of how the disruption has played out over time. To do so, we construct a long-short portfolio of publicly traded non-critical US firms and look at the returns to this portfolio over time.

The unfolding of this COVID-19 factor portfolio largely tracks the unfolding of news related to the pandemic. As of 15 May 2020, this portfolio had lost 50% of its value, relative to a 10% drop for the broad market index – as reopening has begun across the US, that number has recovered to a 35% decline (Figure 2).

Figure 2 Unfolding of the COVID-19 effect on publicly traded non-critical US firms

Notes: This figure shows the time series of the cumulative returns of the COVID-19 factor portfolio relative to the market, accumulated since the beginning of the year.

This portfolio is not only further evidence of the uneven impact of COVID-19, but it also provides a model for how an investor might choose to hedge a portfolio against the economic risks in place. To see which side of the portfolio is driving returns, we bucketed industries into exposure quartiles and looked at their returns (Figure 3). As expected, they sort monotonically with their exposure to supply-side disruptions.

Figure 3 Cumulative returns relative to the market (normalised to 0% on 14 February 2020)

Notes: Cumulative returns for industry portfolios grouped by exposure, relative to the market portfolio, normalised to a return of 0% on February 14, 2020.

Assessing the fiscal policy response

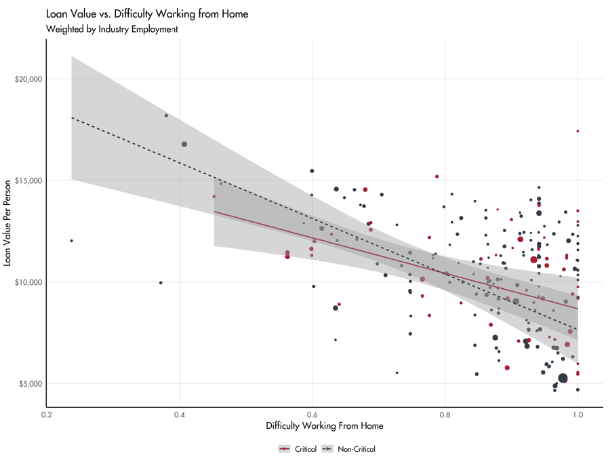

Many governments have responded to COVID-19 with large fiscal interventions. In the US, the government enacted a $669 billion loan programme intended to help smaller firms through the crisis. Recently, the Small Business Administration made data available at the individual loan level, along with estimates of the number of employees.1

The sector that received the largest number of loans (641,000) and the second-highest total amount of funding ($66 billion) was ‘Professional and Technical Services’, which has the highest fraction of workers who can work remotely. If we compare the volume of Paycheck Protection Program loans to the reported employment for participating firms, this amounts to more than $12,400 per employee. By way of contrast, the value of PPP loans per person is only $5,000 and $5,300 in the much harder-hit ‘Accommodation and Food Services’ and ‘Arts, Entertainment, and Recreation’ categories.

The more granular data, summarised in Figure 4, shows striking results: sectors more exposed to the supply-side disruption receive a lower dollar amount per employee than firms in industries that can work remotely, and there is little difference in the treatment of critical versus non-critical industries. A change of one standard deviation in exposure to the disruption is associated with a 19.4% lower loan value in non-critical industries and a 13.2% lower loan value in critical industries.

Figure 4 Loan value vs difficulty working from home

Notes: Loan value per employee vs. difficulty working from home, aggregated at the NAICS4 sector level.

Going forward, we believe that fiscal programmes would be more cost-effective if they targeted the workers and firms in industries most exposed to supply-side disruptions.2 ‘One size fits all’ policy responses may be easy to implement but are likely to fall short in providing effective relief to the most affected sectors.

References

Alon, T M, M Doepke, J Olmstead-Rumsey and M Tertilt (2020), “The impact of COVID-19 on gender inequality”, NBER Working Paper 26947.

Barrero, J M, N Bloom and S J Davis (2020), “COVID-19 is also a reallocation shock”, NBER Working Paper 27137.

Granja, J, C Makridis, C Yannelis and E Zwick (2020), “Did the Paycheck Protection Program Hit the Target?”, NBER Working Paper 27095.

Guerrieri, V, G Lorenzoni, L Straub and W Iván (2020), “Macroeconomic implications of COVID-19: Can negative supply shocks cause demand shortages?”, NBER Working Paper 26918.

Papanikolaou, D, and L D Schmidt (2020), “Working remotely and the supply-side impact of COVID-19”, NBER Working Paper 27330.

Endnotes

1 In the publicly available data, exact loan amounts are not reported for loans above $150,000, and the Small Business Administration reports a range of values the for the dollar amount of the loan. We interpolate the larger loan values using the average of the endpoints for each bin. When aggregating these approximate amounts, we match reported state totals almost exactly (R2 of 0.997). While most firms report their employment, a subset report zero or missing employment totals (distributions of their loan sizes appear to be quite similar to those which report positive employment). We impute these values using the average employment of other firms in the same industry in the same loan size category, though rankings across sectors are essentially unchanged if we assign zero employment instead.

2 Echoing this notion, Granja et al. (2020) find that under the current programme, the most affected regions of the US are not more likely to receive Paycheck Protection Program funding.

"impact" - Google News

July 23, 2020 at 06:06AM

https://ift.tt/2WJ1qTK

The supply-side impact of COVID-19 | VOX, CEPR Policy Portal - voxeu.org

"impact" - Google News

https://ift.tt/2RIFll8

https://ift.tt/3fk35XJ

Bagikan Berita Ini

0 Response to "The supply-side impact of COVID-19 | VOX, CEPR Policy Portal - voxeu.org"

Post a Comment